Dividend Tax 2026/27: Jump to 10.75% Rate and What It Means for You

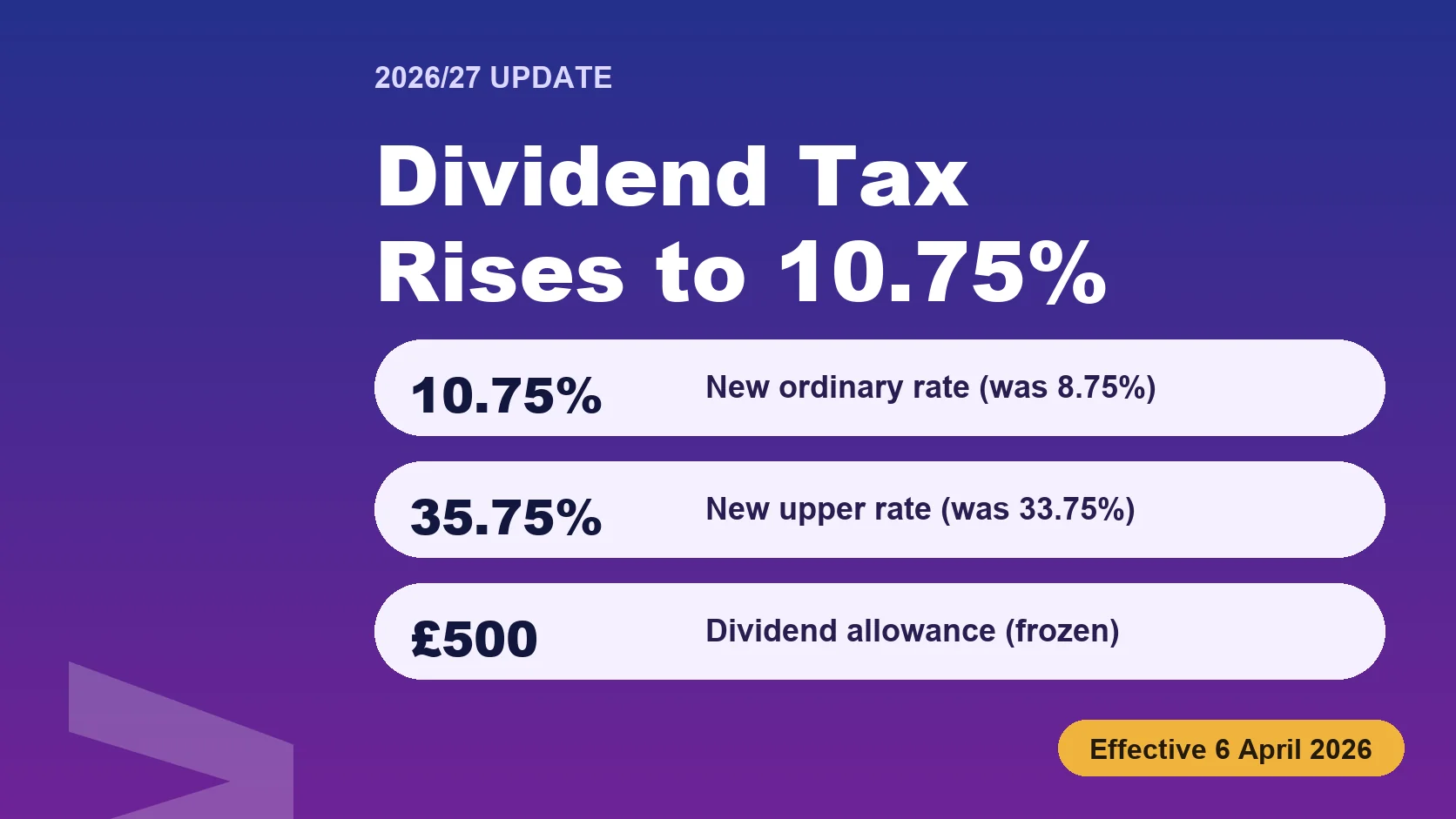

UK dividend tax rates rose on 6 April 2026. The ordinary (basic) rate moved from 8.75% to 10.75% and the upper (higher) rate from 33.75% to 35.75%. The additional rate stays at 39.35%. The dividend allowance remains £500 and the personal allowance remains £12,570. These changes, announced at Autumn Budget 2025, affect every UK director, shareholder, and trustee receiving dividend income in the 2026/27 tax year.

This article is for UK owner-managed limited company directors and their accountants who are planning or reviewing dividend distributions for the 2026/27 tax year. It provides clarity on the upcoming changes and how they impact your financial strategy.

What is changing on 6 April 2026

The following dividend tax rates will increase from 6 April 2026:

- Ordinary (basic) rate: 8.75% rising to 10.75% on 6 April 2026.

- Upper (higher) rate: 33.75% rising to 35.75% on 6 April 2026.

- Additional rate: stays at 39.35% for 2026/27. Only the ordinary and upper rates were increased.

- Dividend allowance: £500, frozen.

- Personal allowance: £12,570, frozen until April 2028.

- Section 455 loans-to-participators charge: continues to track the upper rate, so 35.75% for loans outstanding nine months and one day after the accounting period end where the period ends on or after 6 April 2026.

These changes apply to all dividends with a payment date on or after 6 April 2026, regardless of when the underlying profits were earned.

Who is affected

The new rates apply to anyone receiving dividend income in 2026/27, including:

- Directors and shareholders of owner-managed limited companies taking dividends from their own trading company.

- Family investment companies distributing profits to family members.

- Investors holding listed shares outside an ISA or pension wrapper.

- Trustees chargeable at the dividend trust rate.

Scottish taxpayers are affected on the same terms. Dividend taxation is reserved to Westminster and is not part of the devolved Scottish rate of income tax.

Worked example: £50,000 salary-plus-dividend extraction in 2025/26 vs 2026/27

Consider a sole director taking a £12,570 salary (using the personal allowance) and £37,430 in dividends, bringing total income to £50,000, just below the higher-rate threshold.

2025/26 tax calculation:

- Salary £12,570 sits inside the personal allowance: income tax £0.

- Dividends £37,430 less £500 dividend allowance leaves £36,930 taxable at the ordinary rate of 8.75%.

- Income tax on dividends: £3,231.38.

- Total personal income tax: £3,231.38.

2026/27 tax calculation:

- Salary £12,570: income tax £0.

- Dividends £37,430 less £500 dividend allowance leaves £36,930 taxable at the new ordinary rate of 10.75%.

- Income tax on dividends: £3,969.98.

- Total personal income tax: £3,969.98.

Difference: roughly £738.60 more tax for the same income in 2026/27. Multiply that across a husband-and-wife shareholding and the cost rises proportionately. Employer National Insurance on the £12,570 salary sits on top of this, but the £10,500 Employment Allowance often absorbs it where the company has more than one earner above the secondary threshold.

Salary versus dividend in 2026/27: does the calculus still favour dividends?

While the dividend tax rate increases, the salary tax remains unchanged. However, the employer National Insurance (NI) is still 15% on earnings above £5,000. The Employment Allowance of £10,500 still applies.

If a director takes £12,570 salary and £37,430 dividends, they avoid employer NI on the first £5,000 of salary, and the Employment Allowance can be applied to the full salary if the company qualifies.

The dividend tax increase does not necessarily make salary more attractive, but it does increase the tax burden for those extracting income via dividends.

Try the MBridge Dividend Salary Calculator 2026 →

Three mistakes owner-managed companies make

Mistake 1: Paying dividends from insufficient distributable reserves

Companies must ensure that dividends are paid from distributable profits. If a company has insufficient reserves, paying dividends can lead to personal liability for directors.

Mistake 2: Backdating dividends to chase the old rate

Some directors are tempted to backdate dividend vouchers to before 6 April 2026. The tax point for a dividend is the date it is paid (or, for interim dividends, the date the funds are transferred or credited to the loan account). Backdating board minutes does not change the tax year a dividend falls into and is a serious record-keeping breach.

Mistake 3: Ignoring Section 455 if extracting via loan instead

Directors who take interest-free or low-interest loans from their companies may be subject to Section 455. This tax is linked to the upper dividend rate, which will rise to 35.75% from 6 April 2026.

Practical steps for the rest of 2026/27

- Re-model your salary plus dividend extraction using the new 10.75% and 35.75% rates and the £10,500 Employment Allowance.

- Review remuneration policy for the year, including whether to take any dividends evenly across the year or in larger tranches before crossing the higher-rate threshold.

- Check the directors' loan account position at every month-end. Loans outstanding nine months and one day after the period end attract Section 455 at 35.75%.

- Document distributable reserves before each dividend declaration. A dividend paid without sufficient reserves is unlawful under the Companies Act 2006.

- Plan timing around the higher-rate threshold (£50,270) and the £125,140 additional-rate threshold, since the 35.75% step-up is now larger.

- Update remuneration paperwork: board minutes, dividend vouchers, and shareholder agreements should reference the new rates.

How MBridge helps

MBridge offers a dividend and salary calculator to help you plan your 2026/27 income extraction. The tool accounts for the new rates and can help you model different scenarios.

Read our related post on Section 455 tax on directors' loans for more on how the linked upper-rate change affects loan-account exposure.

HMRC and legislation sources

- Income Tax (Trading and Other Income) Act 2005, Part 4, Chapter 3

- Autumn Budget 2025

- HMRC SAIM5040: Dividend income

- gov.uk: Tax on dividends

- HMRC CTM61500: Loans to participators (s455)

This article is general information current at the time of writing and does not constitute tax or legal advice.

Have a question about this article?

Our team is happy to help with any questions about UK compliance. Get in touch and we will get back to you within one working day.

Ask Us a Question